Taxpayer service traces their origin to the registered agent system established in the United States in 1884. In the 1950s, the U.S. launched its first formal taxpayer assistance initiative, which gave rise to the modern concept of “taxpayer service”. The core connotation is that tax authorities are duty-bound to offer free tax support to taxpayers in diverse ways.

Previously, tax administrations in various countries generally adopted a mandatory management approach, where tax authorities held a dominant position in tax activities, and taxpayers could only passively comply with administrative orders and accept penalties. Taxpayers' tax compliance primarily depended on the intensity of law enforcement and the severity of penalties. This pattern could easily drive taxpayers to evade jurisdiction by all means, thereby intensifying conflicts between tax authorities and taxpayers. In the 1970s, with the rise of the New Public Management movement, government agencies were positioned as providers of public services, making taxpayer service the mission of tax authorities. Meanwhile, the principles of efficiency and equity, the social contract theory of popular sovereignty, and tax compliance theory have also provided theoretical support for the establishment of the taxpayer service philosophy. Research by the International Bureau of Fiscal Documentation also shows that taxpayers prefer positive, service-oriented administrative methods adopted by tax authorities. With the development of relevant theories and the intensification of practical tax collection conflicts, tax authorities around the world have transformed their administrative philosophy from rigid law enforcement to flexible services, placing greater emphasis on respecting and protecting taxpayers’ rights. Accordingly, tax administration has shifted from mere administrative management to service-oriented administration.

To date, both developed and developing countries have either introduced or are in the process of implementing the philosophy of taxpayer service and mechanism that treats taxpayers as "clients" in tax-related activities, aiming to provide taxpayers with high-quality, efficient, and convenient taxpayer service.

From the mid-1950s to the early 1970s, the third scientific and technological revolution—represented by atomic energy, space technology, and electronic computers—along with the emergence of new methodological disciplines such as systems theory, information theory, and cybernetics, not only significantly advanced management modernization but also infused new vitality into the science of public administration. Meanwhile, Western countries were hit by successive social, economic and political crises, which eroded public trust in government. The traditional governance model was no longer capable of stabilizing the situation and addressing prevailing problems. The theory of public administration has also shifted from purely theoretical research to applied research, incorporating numerous theoretical methods and research findings from related disciplines. This shift gave rise to the new public administration theory represented by George Frederickson, Peter F. Drucker's management by objectives theory, and the later-developed entrepreneurial government theory by David Osborne and Ted Gaebler. These theories have significantly influenced Western governments and their administrative practices from various perspectives, with David Osborne's entrepreneurial government theory having particularly far-reaching impact. The entrepreneurial government theory assumes that government entities act in pursuit of their own interests. It advocates that the government unleash market forces to promote individual choice and administrative efficiency, and calls for the privatization of public services by transferring their provision to the market and society. The theory regards citizens as customers, introduces market mechanisms into the public domain to improve service efficiency and quality, and rebuilds government governance through entrepreneurial spirit.

Compared with the traditional public management mode, the new public management theory has the following eight characteristics:

▲ Emphasizing efficiency, results and service quality, the government is no longer a "self-service" bureaucracy, the government civil servants should be responsible "enterprise managers and managers", and the public is the "taxpayer" who provides government tax revenue and the "customer" or "customer" who enjoys government service in return. The government service should be customer-oriented and enhance the responsiveness to the needs of the public.

▲ Replace the highly centralized hierarchical organizational structure with decentralized management, so that resource allocation and service delivery are closer to the supply itself, so as to get more relevant information and feedback from customers and other interest groups.

▲ More flexible alternatives to direct supply of public goods can be explored, thus providing more economical policy results.

▲ Pay attention to the correspondence between authority and responsibility, as the key link to improve performance, including emphasizing a clear mechanism of performance contract.

▲ Create a competitive environment between and within the public sectors.

▲ Strengthen the strategic decision-making capacity of the central government so that it can operate more quickly, flexibly and at low cost, so as to respond efficiently to external changes.

▲ Enhance accountability and transparency by requiring reports on results and overall costs.

▲ Loose service budget and management system support and encourage these changes.

Against the backdrop of the New Public Management movement, public sectors, especially government bodies, have witnessed profound transformations in their functions, roles, status, organizational structures, and social relations, with tax authorities also deeply influenced.

The New Public Management (NPM) Theory and the subsequent NPM theory offer a fresh perspective for tax administration, enabling a re-examination of tax management practices and relationships with taxpayers while providing a theoretical foundation for modern taxpayer service. It not only establishes an equal economic relationship between taxpayers and tax authorities, but also affirms taxpayers' dominant role in the "supply and demand" dynamic of public goods.

Tax authorities around the world have witnessed major shifts in their tax management philosophies and operational models. The transformations are mainly reflected in four aspects: shifting from regulation orientation to service orientation, redefining taxpayers from supervision targets to service recipients, transforming internal management from traditional administration to enterprise-style management, and upgrading taxpayer services from simple administrative services to socialized public services. These reforms are designed to improve overall management efficiency and service quality, so as to adapt to the new requirements of tax administration brought by globalization and the information technology revolution. Government-provided services focus not only on efficiency, effectiveness and performance, but also embody democratic concepts, attaching great importance to civil rights and human respect.

Customer Relationship Management (CRM) Theory originated from Western marketing theories. In 1985, American marketing expert Barbara B. Jackson introduced the concept of relationship marketing, focusing on the management of interpersonal relationships in marketing. The United States pioneered the development of customer relationship management (CRM). In the early 1980s, corporate-customer contact management came into being, which was dedicated to collecting all relevant information on interactions between enterprises and their clients. By 1990, it had further evolved into the customer care system, covering data analysis supported by telephone service centers. Gartner, a leading consulting firm in the United States, emphasized holistic supply chain management when proposing the concept of Enterprise Resource Planning (ERP). Nevertheless, restricted by the inherent functional defects of ERP systems and the immature development of information technology at that time, ERP failed to put forward effective solutions to meet diverse customer demands. By the late 1990s, with the rapid popularization of the Internet, computer telephony integration (CTI) and customer information processing technology achieved substantial progress. This drove the restructuring of corporate organizational structures and business processes, as well as profound changes in the overall social management philosophy. In response to the demands of the new economy and advancements in new technologies, Gartner introduced the concept of customer relationship management.

Customer Relationship Management (CRM) Theory is centered on "customer value management" and views customers as valuable assets to the enterprise. Its core value resides in adopting the one-to-one marketing principle to satisfy personalized demands of differentiated-value customers, enhance customer loyalty and retention, and deliver continuous customer value, so as to comprehensively boost corporate profitability. To achieve this goal, Customer Relationship Management (CRM) Theory sets three core objectives. First, efficiency improvement: realizing information sharing and process automation via information technology to boost internal operational efficiency. Second, market expansion: leveraging new channels such as telephone and the Internet to broaden business coverage and capture market opportunities. Third, customer retention: optimizing customer experience and satisfaction to maintain loyal existing customers and attract new ones.

Customer Relationship Management (CRM) Theory emphasizes implementing "customer segmentation" and "differentiated services." Businesses categorize customers based on factors such as their nature, scale, value, and stage of cooperation—for example, classifying them as potential customers, transactional customers, new customers, existing customers, key accounts, or premium clients. Customer segmentation aims to deliver targeted resource investment under cost control, design differentiated service solutions for customers at diverse value tiers, and realize the matching between service quality and customer value. This helps streamline service workflows and consolidate long-term customer relationships.

The goal of customer relationship management is to be "customer-centric." In light of Customer Relationship Management (CRM) Theory, within the specific scenario of tax governance modernization, it delivers operable methodological guidance for the refined and personalized transformation of taxpayer service. First, it highlights the value of customer information and mandates in-depth customer analysis via information tools, so as to support enterprises in strategy formulation and overall planning. This requires tax authorities to avoid treating taxpayers as a single homogeneous and undifferentiated group. Instead, they shall rely on tax big data to carry out multi-dimensional and three-dimensional categorized management of taxpayers. For example, based on information such as enterprise scale, industry, credit rating and historical tax-handling behaviors, China's tax authorities precisely categorize taxpayers into different groups, including large enterprises, small and medium-sized enterprises, high-compliance taxpayers and specific-risk taxpayers, and allocate differentiated tax collection and management resources and adopt targeted service strategies accordingly. Second, it emphasizes using technical means to provide personalized services for customers, thereby enhancing customer loyalty. This indicates that tax authorities can conduct taxpayer segmentation and behavioral insight analysis to precisely push targeted tax and fee policies, risk warnings and dunning notices, tailor tax handling guidelines, and deliver on-demand and personalized precise services. For example, the Korea National Tax Service has launched the "Home-tax" platform, which applies an artificial intelligence-driven search engine to understand taxpayers’ plain-language inquiries and send personalized reminders according to individual user situations. In 2024, South Korea launched an AI-enabled tax hotline. Supported by voice recognition technology, it provides consulting services and instantly shares links to FAQs, operational guidelines and relevant materials throughout the call. Third, it emphasizes customer satisfaction as the key metric for measuring service performance. Through taxpayer satisfaction survey and systematic collection and analysis of user feedback, tax authorities can incorporate public service perception data into service process improvement and organizational performance assessment. For example, the Canada Revenue Agency implemented a feedback tool on its official platform to gather user suggestions for system optimization. Using generative artificial intelligence, it analyzed and summarized 90,000 comments, identifying 10 key areas for improvement. This ultimately led to a 158% increase in user operation success rates.

With the emergence of taxation, a distinction arises between tax compliance and non-compliance. Tax compliance is defined as taxpayers’ voluntary obedience to tax laws, driven by their recognition of the value of national tax rules or trade-offs of personal interests. Tax non-compliance is defined as taxpayers’ failure to abide by tax regulations, regardless of whether such conduct is intentional or unintentional.

Haig, an American scholar, was the first to study tax compliance costs. In 1934, he pioneered research on tax compliance costs of U.S. federal and state taxation, yet failed to put forward a clear definition for this concept. Subsequently, relevant studies on tax compliance costs have been continuously enriched. Until the 1980s, Cedric Sandford, Professor at the University of Bath, made fruitful achievements in tax compliance cost research, after which systematic research on tax compliance officially emerged. Taking taxpayers’ tax behaviors and decisions as its research objects, tax compliance theory embodies the contemporary traits of focusing on individual differences, highlighting individual interests, as well as respecting and safeguarding taxpayers’ legitimate rights.

Studies on tax compliance theory demonstrate that:

▲ Tax authorities must provide standardized taxpayer services to fully fulfill tax administration objectives.

▲ The optimization and upgrading of taxpayer service serve as the fundamental approach to reducing tax compliance costs.

The primary objective of taxpayer service is to maximize tax compliance. The management of tax compliance should encompass at least two aspects: First, having a clear understanding of taxpayers and being able to classify them appropriately; Second, developing targeted management measures based on these classifications to encourage and guide taxpayers in maintaining a state of voluntary compliance.

In practice, tax authorities can analyze the motivations behind taxpayers' non-compliance based on the tax compliance influencing factors model. This enables the design of differentiated service strategies to guide taxpayers from "passive compliance" to "active compliance."

For example, to address non-compliance caused by taxpayers' lack of comprehensive understanding of tax policies and regulations, China's tax authorities have widely implemented a "targeted taxpayers policy delivery" service for tax policies. Leveraging tax big data, they conduct "profile" analyses of taxpayers and proactively provide new businesses with a "first lesson for new businesses" guidance package, which includes tax filing procedures, common error examples, and enquiry channels. This initiative has increased the on-time filing rate for new businesses' first tax declarations to over 96%.

To address non-compliance resulting from high tax filing costs, Australia launched the Standardized Business Reporting (SBR) program in 2006. This initiative consolidates reporting requirements from 12 government agencies, including taxation, statistics, and regulatory bodies. The number of data elements companies must report was reduced from 9,648 to 2,838, cutting over 70% compliance burdens and saving approximately AUD 800 million annually for society.

To address non-compliance stemming from a lack of trust in tax authorities, the Australian Taxation Office introduced the "Verify Call" feature in its official app in April 2026. When taxpayers receive a call claiming to be from the tax office, they can use the app to verify the call's authenticity and will receive a system notification within 30 seconds. In July 2025 alone, the ATO received nearly 7,500 reports of scams impersonating tax officials.

"Taxpayer-centric" is the fundamental value upheld by China's tax authorities in advancing the modernization of tax governance. In 2008, at the "Taxpayer Service and Tax Compliance" forum hosted by The Chinese Tax Institute and other institutions, the new concept of "taxpayer-centric" taxpayer service was explicitly introduced for the first time. This marked the official shift in China's tax administration from the traditional "control-oriented" approach to a modern "service-oriented" model. The introduction of this concept reflects both a reconsideration and transcendence of the long-standing power-centric mindset in tax administration, as well as a concrete manifestation and value extension of the Chinese government's "people-centered" development philosophy in tax collection and payment processes. It marks a gradual shift in the role of China's tax authorities from mere regulatory enforcers to providers of public services. In 2015, the General Office of the CPC Central Committee and the General Office of the State Council issued the Plan for Deepening the Reform of the National and Local Tax Collection and Management Systems. This marked the first time the "taxpayer-centric" approach was formally incorporated into a central government top-level reform document, elevating this concept from a departmental-level work initiative to a policy principle at the national governance level. The top-level design provided robust institutional legitimacy to support this principle.

The evolution from value declaration to institutional recognition demonstrates that the "taxpayer-centric" service philosophy is not merely an operational guide for optimizing taxpayer service, but also the core value pivot driving tax administration from a power-based to a responsibility-based approach, and from a control-oriented to a service-oriented model. This concept provides a fundamental theoretical foundation for advancing the modernization of the tax governance system and its capabilities.

With the continuous development and enrichment of theories, countries around the world have generally incorporated taxpayer service into the core framework of tax administration. The U.S. Internal Revenue Service has clearly defined its mission as "providing the highest quality service to taxpayers" and its philosophy as "serving every taxpayer and all taxpayers"; the Canada Revenue Agency defines its mission as "delivering quality services to support Canada's economic and social development"; the Brazilian Federal Revenue Service has established its mission as "providing optimal tax services to society"; while China's tax authorities have set their mission as "beginning with taxpayer needs, grounded in taxpayer satisfaction, and culminating in taxpayer compliance," among others. Based on the fundamental principle and noble mission of serving taxpayers, countries have gradually established a comprehensive taxpayer service system that encompasses systems and mechanisms, methods and approaches, as well as evaluation and supervision, thereby standardizing taxpayer service practices.

The Introduction and Refinement of China's Taxpayer Service Philosophy

China's taxpayer service has been continuously evolving and innovating, generally progressing through three stages: the introduction and establishment of taxpayer service philosophy, the initial development and exploration of taxpayer service, and the advancement and refinement of taxpayer service.

Figure1: The Development of Taxpayer Service in China

(1)The Development of Taxpayer Service in China

▲Phase One: Introduction and Establishment of Taxpayer Service Philosophy (1990–2001)

In 1990, the National Tax Administration Conference proposed that "the tax administration process should be viewed as a service process for taxpayers."

In 1997, the "Plan for In-Depth Tax Administration Reform" was approved, formally establishing a new tax collection model based on "declaration and optimized services, supported by computer networks, with centralized collection and focused inspections."

In 2001, the revised and reissued the Law on Tax Collection and Administration of the People's Republic of China established "serving taxpayers" as a key responsibility of tax authorities, defined the rights and obligations of both tax authorities and taxpayers, and formed the legal foundation for taxpayer service.

▲Phase Two: Initiation and Exploration of Taxpayer Service (2002–2007)

In 2002, State Taxation Administration established a Taxpayer Service Division within its Revenue Management Department, creating a dedicated planning and administrative body for taxpayer service in China. This division is responsible for overseeing taxpayer service administration across the national taxation system.

In 2005, State Taxation Administration issued the "Standards for Taxpayer Service (Trial Implementation)," which established clear regulations for taxpayer service in various aspects of taxation work, including tax collection, management, inspection, and the implementation of tax legal remedies.

In 2007, the first National Taxpayer Service Conference was held, marking the first comprehensive deployment of taxpayer service initiatives and signifying that taxpayer service had become a nationwide priority for China's tax authorities.

▲Phase Three: Development and Improvement of Taxpayer Service (2008–present)

In 2008, State Taxation Administration established the Taxpayer Service Department, responsible for organizing, managing, and coordinating nationwide taxpayer service, marking a new chapter in China's taxpayer service development. Since then, China's taxpayer service has entered a phase of rapid advancement.

Since 2014, State Taxation Administration has annually launched the "Spring Breeze Campaign for More Convenient Taxation Service," focusing on addressing issues in taxpayer service awareness, administrative streamlining, operational efficiency, and standardized law enforcement. This initiative has successfully achieved its objectives by identifying key challenges, overcoming bottlenecks, continuously improving services, and effectively reducing taxpayers' compliance burdens, establishing itself as a outstanding brand in tax service innovation.

In 2014, the "National Tax Service Standards for County-Level Tax Authorities (Version 1.0)" were implemented nationwide. The focus is on service items requested by taxpayers, while also appropriately considering service and management activities conducted by tax authorities under their jurisdiction. Additionally, it includes requirements for courteous services such as service locations, methods, and language, reflecting a taxpayer-centric service philosophy that treats taxpayers as valued clients. Subsequent releases and gradual upgrades to versions 2.0 and 3.0 provided effective institutional support for tax authorities at all levels to deliver taxpayer service in a standardized and consolidated manner.

In 2018, the "Tax Service Halls Integration Work Plan" and the "12366 Taxpayer Service Integration Work Plan" were issued, implementing comprehensive "one-stop service" and "one-call enquiry" across China's tax system. This initiative gradually enabled taxpayers to complete all procedures by visiting a single hall, approaching one counter, making one call, and dealing with one tax official.

In 2021, China's tax authorities advanced reforms to facilitate tax and fee payments by streamlining processes, promoting "non-contact" taxpayer services through E-Tax China, mobile apps, and self-service terminals. They expanded online payment options, introduced diversified methods including third-party payments, and continuously improved the convenience of tax and fee transactions.

In 2026, State Taxation Administration issued the "Implementation Plan for Further Advancing the New Tax and Fee Service System (2026-2027)," upholding a people-centered development philosophy with the goal of enhancing compliance. Through establishing integrated 12366 services, upgrading the complaint resolution mechanism, deepening the integration of management and services, and actively engaging with the social governance system, the administration will advance the "Strengthening Foundations Project" service measures. This initiative will transform tax and fee services into a more proactive, streamlined, and intelligent model, ensuring more efficient operation of the new service framework. These efforts will contribute to building a fair, rule-of-law-based taxation environment and fostering a compliance-driven tax governance ecosystem.

Taxpayer service starts with the awakening of concepts and is perfected through the institutionalization of systems. In the process of transitioning tax governance from a "management-oriented" to a "service-oriented" approach, countries (regions) have gradually recognized that high-quality taxpayer service is not only a requirement for tax authorities but also a legal right of taxpayers. However, with only advocacy of ideas with no legal backing, service commitments can easily become mere slogans, and taxpayers' rights and interests lack stable protection. Therefore, elevating the taxpayer service philosophy to legal standards and ensuring its enforcement through state authority has become a key aspect of improving taxpayer service quality.

Establishing a comprehensive legal framework for taxpayer service holds significant practical importance: First, it helps define the boundaries of rights and obligations, ensuring clarity in the service responsibilities of tax authorities and the procedural rights of taxpayers. Second, it strengthens the enforceability of rights relief, such as through taxpayer assistance orders and administrative appeal systems, providing effective legal safeguards when taxpayer rights are infringed. Third, it standardizes service norms to prevent declines in service quality due to personnel changes or subjective variations.

The following three models can be adopted to integrate taxpayer service into the legal safeguard system: First, the rights and obligations of taxpayers, along with the fundamental principles of taxpayer service provided by tax authorities, should be enshrined in the national constitution to ensure the protection of taxpayers' rights under the country's fundamental law. Second, specific requirements for taxpayer service should be incorporated into administrative regulations, local regulations, local government rules, and other provisions, with operational standards refined through administrative legislation. For example, Kazakhstan's new Tax Code, which will take effect in 2026, focuses on streamlining administrative procedures by emphasizing "reminder-based" off-site audits and simplifying the debt collection process. The third approach is to adopt a standalone legislative model, establishing Rights and Obligations of Taxpayers through specialized laws or charters. For example, the U.S. Congress passed the Taxpayer Bill of Rights in both 1988 and 1996, which not only established an independent Office of Taxpayer Rights Protection but also authorized it to issue legally binding "Taxpayer Assistance Orders" to provide timely relief when taxpayers face significant hardships. Australia has implemented the Taxpayer Charter since 1997, clearly defining key taxpayer rights, including fair treatment, privacy protection, and timely enquiry, thereby transforming service commitments into statutory safeguards. China's 2001 revision of the Law on Tax Collection and Administration explicitly designated taxpayer service as a statutory responsibility of tax authorities, providing a direct legal foundation for establishing a service-oriented tax governance system.

The intervention of legal safeguards ensures that taxpayer service is no longer limited to moral self-discipline or policy advocacy but instead become a legal obligation that tax authorities must fulfill and a substantive right that taxpayers can claim under the law. This institutionalized arrangement fundamentally drives the transformation of tax administration from one-way mandatory management to two-way compliance, helping to establish a solid legal foundation for fostering harmonious relations between taxpayers and the tax administration and optimizing the tax business environment.

Ethiopia introduces a Customer Charter to standardize taxpayer service

Ethiopia has a customer charter that clearly defines the rights and obligations of both taxpayers and tax authorities in daily operations. To improve service efficiency, the authority’s research and development team conducts regular customer satisfaction surveys to assess service quality and roll out targeted improvements.

To enhance tax collection and administration efficiency, tax authorities in various countries have implemented significant reforms in their organizational structures, focusing on improving efficiency and service delivery. Generally speaking, there has been a gradual transition from the early "tax type" model (categorized by tax type) to a primarily "functional" division, where personnel are organized and functional departments are determined based on business function classifications (such as registration, declaration, collection, audit, accounting, and appeals). This institutional setup effectively addresses the issues of functional overlap, inefficiency, and multiple handling points for taxpayers under the "tax category" model. It professionalizes cross-tax procedures while enhancing the quality and effectiveness of tax administration performance management. However, this model also has its own limitations and shortcomings. For example, functional subdivision can easily lead to poor service coordination and inconsistent implementation standards. Additionally, it lacks a flexible response mechanism for taxpayers' mixed tax filing behaviors and varying compliance attitudes.

Therefore, in recent years, western developed countries (such as Australia and the United States) have introduced a new organizational model—the taxpayer group or type model. This model primarily organizes tax authorities services and functions based on different taxpayer groups (e.g., large enterprises, small and medium-sized enterprises, high-net-worth individuals, etc.). It promotes streamlined management levels and is more conducive to implementing risk management and providing personalized services tailored to the characteristics and tax compliance behaviors of different taxpayer groups.

According to the OECD survey of 52 countries in 2013, countries and territories including Australia, the United States, the United Kingdom, Ireland, and France have adopted an organizational model for tax agencies based on taxpayer categories. Meanwhile, countries such as Austria, Germany, and Mexico have implemented a hybrid organizational structure that combines taxpayer categories with functional divisions. Tax authorities in 44 countries have established specialized internal departments to handle tax matters for large enterprises. In addition, many governments have established specialized agencies to handle complaints arising from administrative actions between government agencies (including tax authorities) and citizens or enterprises. Among the 52 countries and territories surveyed, 18 have tax authorities with ombudsman offices or equivalent agencies responsible for addressing taxpayer complaints (including non-tax-related complaints). 10 have set up dedicated agencies specifically to handle complaints from citizens and enterprisess regarding actions or inactions by tax authorities. Another 5 have established independent departments within their tax authorities to process taxpayer complaints.

Based on the practices of taxpayer service departments worldwide, the organizational forms of taxpayer service can generally be categorized into the following 2 approaches:

At the central tax authority level, an independent taxpayer service agency should be established to separate core taxpayer service functions from tax administration departments, with an independent organizational structure and clearly defined powers and responsibilities. Under this model, the taxpayer service function is supported by a well-defined institutional framework, independent resource allocation authority, and systematic coordination capabilities, enabling more precise and professional responses to taxpayers needs.

China establishes specialized taxpayer service agencies

After years of continuous reform and improvement, China's taxpayer service system has established an organizational structure with clear hierarchies, coordinated operations, and complementary functions. Overall, taxpayer service agencies have evolved from nonexistence to establishment, from decentralization to centralization, and from single-function operations to comprehensive services, providing solid organizational safeguards for optimizing the tax business environment and safeguarding taxpayers' legitimate rights and interests.

▲ At the State Taxation Administration level

In 2008, China's State Taxation Administration established the Taxpayer Service Department as its overarching functional division responsible for taxpayer service. This department organizes and implements the taxpayer service system, formulates service standards and operational procedures, coordinates tax counseling, enquiry services, and legal relief efforts while handling taxpayer complaints. It oversees the development of the tax credit system, conducts mediation in tax disputes, and drafts the implementation of tax agent management policies. There are 7 internal departments: General Affairs Office, Tax-related Service Supervision Office, Tax Law Publicity Office, Tax Filing Office, Taxpayer Rights Protection and Business Environment Office, Tax Credit and Service Standardization Management Office, and Small and Micro Enterprises Service Office.

In 2015, in accordance with the deployment and requirements outlined in the "12366 Taxpayer Service Upgrade Plan" by the State Taxation Administration, the 12366 Beijing Taxpayer Service Center was officially established. This transformed the center into a comprehensive national-level taxpayer service hub with "six core functions": enquiry, search, viewing, listening, reserving, and processing capabilities.

In 2016, the State Taxation Administration established the 12366 Shanghai (International) Taxpayer Service Center in Shanghai. 12366 Shanghai Center focuses on the four main functions of "supporting national development strategies, fostering international exchange and cooperation, innovating taxpayer service branding, and enriching tax culture experiences." It is dedicated to building a comprehensive taxpayer service platform that integrates international, intelligent, and digital features. It has successively introduced a series of international tax and fee taxpayer service initiatives, including the China International Tax Service Hotline, English Intelligent Consulting Service, and 12366 Multi-Language and Multi-Channel Tax and Fee Enquiry Service System. Leveraging big data and artificial intelligence technologies, it conducts enquiry data analytics and collects taxpayer feedback, while exploring innovative models such as "preemptive responses" and "proactive resolution" to continuously enhance the intelligence of taxpayer service.

▲ At the provincial tax authorities level

In 2018, with the advancement of tax administration reform, taxpayer service agencies below the provincial level were further strengthened. Provincial and municipal tax authorities have established taxpayer service divisions (sections) and taxpayer service centers. The county tax authorities have established taxpayer service divisions (sections) and the first tax branches (offices), continuously improving taxpayer service agencies and expanding the taxpayer service workforce.

In 2024, in accordance with the fiscal and tax system reform requirements, agencies will be streamlined by abolishing county-level taxpayer service departments (units). This restructuring further optimizes the functional allocation of local tax authorities, enhances the efficiency and specialization of taxpayer service, and ensures more unified and effective service delivery after the organizational adjustments—better meeting the needs of taxpayers and contributors.

At the central tax authority level, no dedicated taxpayer service department is established separately. Instead, taxpayer service functions are integrated into internal functional divisions or business units categorized by tax type or taxpayer categories. This ensures seamless coordination between service processes and enforcement procedures such as tax collection and inspection during daily operations. In this model, taxpayer service is not neglected or weakened but is integrated into every aspect of daily tax administration, operating smoothly within the existing organizational framework. For example, all business departments of the Inland Revenue Authority of Singapore (IRAS) may independently formulate and implement special service plans and conduct public outreach activities within their respective jurisdictions.

Organizational Structure and Functional Division by Business Category in Indonesia

The Indonesian Tax Administration is a department under the Ministry of Finance responsible for tax collection and management. Its main divisions include:

▲ General Office of the State Taxation Administration

The Office of the State Taxation Administration is responsible for developing and implementing tax policies, establishing standardized tax systems and procedures, providing technical guidance and oversight on taxation matters, and conducting tax monitoring, evaluation, and reporting.

The Office of the General Administration of Taxation comprises the Secretariat of the General Administration, the First Bureau of Tax Regulation, the Second Bureau of Tax Regulation, the Bureau of Inspection and Settlement, the Bureau of Law Enforcement, the Bureau of Assessment, the Bureau of Objections and Appeals, the Bureau of Compliance Review, the Bureau of Enquiry, Services and Public Relations, the Bureau of Information Technology, the Bureau of Internal Compliance and Human Resources, the Bureau of Communications and Information Technology, the Bureau of Business Processes, the Bureau of International Taxation, and the Bureau of Tax Intelligence. These departments collectively carry out the functions of the General Administration of Taxation and perform additional duties as assigned by the Minister of Finance.

▲ Tax Data and Document Processing Center: Utilizes information technology for receiving, scanning, recording, and storing tax documents.

▲ Jakarta Special Tax Regional Office: Coordinates, guides, controls, analyzes, and executes tax-related tasks, while implementing relevant tax policies for Large Enterprises (primarily including large-scale enterprises, foreign-invested enterprises, and listed companies).

▲ Regional offices of the State Taxation Administration: Coordinates, guides, controls, analyzes, and executes tax-related tasks while implementing policy directives from the Central Office.

▲ Large Enterprise Tax Office: Collects information, provides taxpayer services, and conducts tax supervision for large enterprises, foreign-invested enterprises, and listed companies that meet a certain scale threshold.

▲ Tax Commissioner's Office: Provides tax enquiry, services, and oversight for individual taxpayers and taxpayers not under the jurisdiction of the Large Enterprises Tax Office.

▲ Tax Advisory Office: Provides tax services and enquiry support for taxpayers in remote areas.

A robust taxpayer service institutional guarantee system is the foundation for an organization's stable operation. A well-established system can solidify organizational experience, foster a service culture, stabilize service expectations, and contribute to maintaining positive relations between taxpayers and the tax administration.

Taxpayer service fall under the category of basic public services. In accordance with the principle of equalization, taxpayers across different regions, scales, and industries are all recipients of basic public taxpayer services, and tax authorities should treat them equally and fairly. Under the principle of equalization, tax authorities should establish unified taxpayer service standards, detailing service criteria and operational guidelines. They must specify the requirements for each step—from taxpayer enquiries, business acceptance, document review, and case processing to result feedback—while standardizing service language, procedures, and timelines. This ensures taxpayers receive consistent and standardized service experiences across different regions, tax offices, and service channels.

On the basis of ensuring standardized and unified service procedures, clear constraints should also be established for the conduct and ethics of tax officials. The Code of Conduct falls under the purview of professional ethics management. In accordance with the principles of transparency and accountability, all tax officials must adhere to uniform standards regarding professional ethics, work discipline, integrity, and compliance to ensure consistent and fair implementation of these standards. Tax authorities must establish detailed performance standards for their officials, clearly defining conduct guidelines and prohibitions at every stage—from client interactions and service delivery to policy explanations and emergency response. They should unify professional discipline requirements and integrity standards, uphold values of impartial enforcement and efficient service, and safeguard taxpayers' legitimate rights. Strict protection of tax-related trade secrets and personal privacy must be ensured, guaranteeing that taxpayers receive both reliable procedural convenience and professional, trustworthy service throughout tax interaction.

As a key aspect of new public management, government agencies' performance evaluation carries the significant responsibility of enhancing government accountability and operational efficiency. Taxpayer service performance evaluation is an important component of government performance assessment. It not only clearly defines the objectives and direction of government taxpayer services, but also facilitates public oversight, enabling the government to better fulfill its public responsibilities.

Each country (region) should establish a multi-level, multi-indicator taxpayer service performance evaluation and review system based on its specific circumstances. The evaluation system design should adhere to the principles of openness, fairness, impartiality, and objectivity, conducting a comprehensive assessment of taxpayer service quality across four dimensions: economy, efficiency, effectiveness, and equity. The evaluation content may include elements such as overall objectives, performance goals, and reference indicators.

Specifically, the evaluation process must adhere to the following principles: First, it should be targeted and focused, conducting performance assessments of core taxpayer service operations while also incorporating performance evaluations of taxpayer rights protection efforts. Second, it should be both practical and forward-looking. While determining the performance evaluation of key taxpayer service objectives for the current period based on the specific work arrangements of the tax authorities, we must also steadily advance the phased implementation of medium- to long-term taxpayer service development goals.

In addition, it is necessary to establish an incentive and restraint mechanism that links performance evaluation results with individual assessments of tax officials and adjustments to departmental resource allocation. Institutions and individuals with outstanding evaluations should be commended and rewarded, while those with identified issues should be promptly addressed and corrected. This will create a virtuous cycle of "evaluation—feedback—improvement—enhancement." Continuously inspire the tax authorities to pioneer and innovate, and strengthen the internal drive of tax officials to improve services.

Taxpayer service departments should not only focus on building and improving the assessment system in which they serve as the primary evaluators, but also emphasize public participation, communication, and feedback. This includes recognizing the role of individual citizens, social groups, media organizations, and intermediary assessment agencies in evaluating and monitoring government performance through various means. These external evaluations and oversight help leverage the role of diverse assessment entities while conducting self-evaluations, enhancing the quality of taxpayer service performance assessments through increased social supervision and management.

In terms of specific practices, the tax authorities can further improve the external supervision mechanism by taking the following steps: First, establish a regular taxpayer satisfaction survey and follow-up system to periodically gather feedback and suggestions from taxpayers through online and offline questionnaires, on-site evaluations at taxpayer service halls, phone follow-ups, and other methods, while incorporating the evaluation results into performance assessments. Second, streamline diversified oversight channels by leveraging enquiry service hotlines, electronic interactive platforms, tax-related media comment sections, and other means to establish a "service supervision" column. This ensures timely acceptance, processing time limits, and transparent feedback for public complaints and suggestions. Third, independent third-party evaluation agencies will be introduced to conduct regular professional assessments of taxpayer service quality and efficiency, publish evaluation reports, and proactively disclose them to the public. Fourth, proactively welcome oversight from news media and online public opinion by organizing events such as "Tax Open Days" and media roundtables, where reporters and taxpayer representatives are invited to experience the tax filing process firsthand and provide suggestions for improvement. Fifth, leverage the bridging role of social organizations such as industry associations and chambers of commerce to gather common industry demands and drive targeted service optimization.

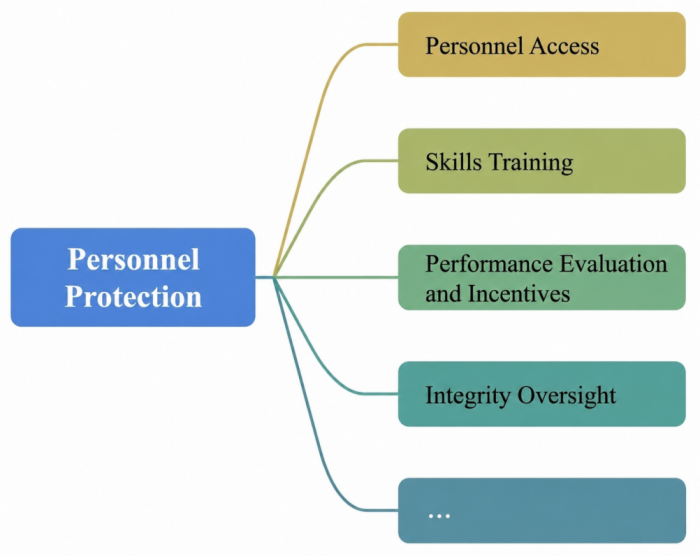

Taxpayer service should focus not only on optimizing business processes and upgrading systems, but also on ensuring adequate staffing for service providers. This includes comprehensive support measures such as professional skills development, career advancement opportunities, psychological counseling services, and positive incentive programs. These people-oriented measures help stimulate internal motivation, strengthen the foundation of services, and thereby enhance overall service capabilities and public satisfaction.

Figure2: Taxpayer Service Personnel Protection

Tax authorities should establish and improve a multi-tiered and refined human resource allocation and support mechanism for taxpayer service based on local conditions. The allocation of taxpayer service personnel should follow the principles of matching personnel to positions, scientific coordination, and dynamic optimization. Specific personnel support measures should be implemented in 3 areas: qualification requirements, staffing approvals, and dispatch response. The content may include job qualification standards, staffing criteria, and flexible deployment methods, among others. It should emphasize both relevance and adaptability, specifying professional competency requirements for frontline taxpayer service positions while also addressing human resource arrangements for emerging online service models and service guarantees for vulnerable groups. Additionally, it should balance practicality and foresight by scientifically determining current service staffing levels based on trends in regional taxpayer numbers, tax source structures, and business complexity. As online service demand grows, timely adjustments should be made to position layouts to continuously optimize the structure of the taxpayer service workforce, thereby maximizing the ability to meet taxpayers' diverse and personalized taxpayer service needs.

The tax authorities should design differentiated training content and paths for taxpayer service personnel at different levels and positions. For new hires, the focus is on fundamental regulations, process standards, and service etiquette; for key personnel, they enhance policy analysis, complex issue resolution, and demand insight; for management roles, team coordination and strategic competency are the emphasis. The training methods should be flexible and diverse, incorporating various approaches such as case studies, scenario simulations, role-playing, on-site observations, and online learning. Tax experts and service role models should be invited to conduct lectures and share their expertise. Additionally, a feedback mechanism for training effectiveness evaluation should be established, linking training outcomes to career advancement and performance assessments.

The tax authorities should improve the performance evaluation mechanism for taxpayer service, incorporating key indicators such as taxpayer satisfaction, service efficiency, operational accuracy, and complaint resolution timeliness into the assessment framework, while appropriately allocating the weighting of these metrics. The assessment should adopt an approach that integrates process evaluation with outcome verification, supplements quantitative scoring with qualitative assessment, and fully incorporates taxpayers' feedback. For those with outstanding performance, positive incentives such as public commendation, honorary titles, priority promotion, and material rewards will be granted. For those who rank low in evaluations or commit service misconduct, appropriate measures—including counseling sessions, position adjustments, probationary training, or even disciplinary actions—will be implemented. This establishes a clear principle of rewarding excellence and penalizing shortcomings, effectively motivating tax personnel to enhance service quality through intrinsic drive.

The tax authorities shall focus on enhancing the professional ethics of taxpayer service personnel and firmly establish a sense of responsibility to perform duties in accordance with the law and serve the public. Enhance the internal control system for integrity risks, implementing effective oversight and checks and balances for key aspects such as discretionary authority and external interactions within the service process. At the same time, it is essential to ensure the accessibility and responsiveness of reporting and complaint channels, encourage taxpayers to provide oversight and feedback regarding taxpayer service conduct and ethical standards, and impose disciplinary actions on verified violations or misconduct to effectively uphold the integrity and impartiality of the taxpayer service workforce.

A standardized and transparent funding management mechanism is essential for ensuring the effective performance of taxpayer service functions and the rational allocation of service resources. The management of taxpayer service funds encompasses budget preparation, expenditure control, supervision, and evaluation. The core objective is to enhance the positive correlation between fund utilization efficiency and service quality.

The budget preparation process must adhere to the principles of balancing income and expenditures, comprehensive planning, and prioritizing key areas. Based on the medium- and long-term planning and annual work arrangements for taxpayer service, it should conduct scientific calculations and reasonable prioritization of funding requirements for various service projects. The budget preparation process should incorporate the concepts of rolling budgets and performance-based budgeting, enhance forward-looking projections for key reform initiatives and routine operational support, and align funding allocations with the development stage of taxpayer service, business scale, and taxpayer expectations. In addition, a dynamic budget execution adjustment mechanism should be established to effectively address temporary and emergency service support needs, thereby further improving the scientificity and applicability of budget allocations.

A clearly defined expenditure scope is the prerequisite for standardizing fund usage. The allocation of taxpayer service funds should prioritize core business areas directly related to taxpayer services, including but not limited to: producing and distributing tax policy publicity and enquiry materials, daily operation and maintenance as well as functional upgrades of taxpayer service halls, building and providing technical support for information service platforms, professional training for frontline service personnel, and conducting taxpayer satisfaction surveys and needs assessment activities. On the basis of clearly defining expenditure boundaries, practical expenditure standard guidelines should also be established to regulate the scope, limits, and approval procedures for various expenses. This will effectively prevent arbitrary use of funds and ensure that fund allocation aligns with service objectives.

A robust oversight system is a critical line of defense for ensuring the security and efficiency of funds. In terms of internal management, a comprehensive oversight mechanism should be established to cover the entire process—from pre-approval and real-time monitoring to post-expenditure evaluation of fund usage. Through regular internal audits and special inspections, issues such as budget execution deviations or non-compliant expenditures should be promptly identified and corrected. In terms of performance evaluation, the actual effectiveness of fund utilization can be assessed by linking financial inputs with service outputs (such as improvements in tax processing efficiency and changes in taxpayer satisfaction). For issues identified during supervision, clear procedures for tracking rectification and assigning responsibility should be established to ensure funds are used for their designated purposes and to prevent resource stagnation or inefficient utilization, thereby continuously enhancing the overall effectiveness of taxpayer service funding.

The United Arab Emirates Orderly Allocation of Taxpayer Service Department Resources

The Federal Tax Authority (FTA) ensures the effective delivery of its Taxpayer service functions through a dedicated Taxpayer Services Department (“TPS”) operating within a clearly defined organisational and governance framework. TPS forms a key component of the FTA’s overall mission, vision and related compliance strategy. TPS’s mandate is developed to deliver against the primary objective of supporting voluntary Tax compliance, improving Taxpayer Certainty, providing Taxpayer Guidance, and reducing to even eliminating the administrative burden in the interactions with the FTA across Tax Procedures and all Tax types in the UAE.To fulfill the above responsibilities, TPS has implemented specific measures in the following key areas:

In terms of personnel support, newly joined TPS Officers are required to follow-up an onboarding training plan and are included in the ongoing TPS Department training schedule (modules include Legislative updates, Tax Technical topics, Emaratax navigation and Taxpayer interaction skills). This ensures high levels of technical knowledge, service consistency and overall professionalism.

In terms of resource requirements and planning, operational demand, legislative developments, and strategic priorities are proactively and efficiently addressed in collaboration with the FTA HR Department.

In terms of budget, budgets are allocated to the TPS Department and a specific budget request process for specific projects and services is implemented.

In the future, the development of taxpayer service will continue to uphold the "taxpayer-centric" service management philosophy, deeply integrating digitalization, intelligence, and internationalization trends. Leveraging digital technologies such as cloud computing, blockchain, and artificial intelligence, it will establish an intelligent tax system offering features and services including automated tax aggregation, proactive enquiry response, multilingual AI assistants, and precise tax policy dissemination. This will enhance tax compliance and taxpayer experience while supporting the optimization of the global business environment.